As the UK mortgage market emerges from the first half of 2025, our latest Mortgage Market Briefing reveals clear signs of renewal. With mortgage rates falling by 62 basis points year-on-year, borrowers are now saving an average of £888 annually. Demand is reawakening, with applications up 9% on the previous year. Fixed‑rate lending continues to dominate, but shorter-term deals are gaining popularity with borrowers.

Commenting on July’s findings, Rob Clifford, Stonebridge Chief Executive, said, “After a bruising couple of years, the mortgage market is starting to find its feet again, with falling rates boosting activity and giving a much-needed confidence boost to borrowers.

“Applications jumped 9.2% in July compared with a year ago, proof that cheaper borrowing is starting to grease the wheels of the market. The average rate on new loans has dropped to 4.44% – 62 basis points lower than last July. While mortgage rates remain much higher than they were a few years ago, the fall over the past 12 months has been meaningful. On a typical 25-year term, that’s worth around £890 a year back in borrowers’ pockets.

“With the potential for two further rate cuts this year, the market should continue its recovery in the second half of 2025. We’re not back to the boom times, but compared with where we were 12 months ago, this is a much healthier market.”

Fixed vs. Variable

“Fixed rates still rule the mortgage market, with 96% of new borrowers opting for the certainty they offer in July – virtually unchanged from a year ago. It’s a clear sign that borrowers are prioritising stability over marginal savings that may never appear.

“Even though tracker rates are once again cheaper than fixed deals, the gap is too small to tempt most people away from the security of a fixed monthly payment. When fixed rates are this cheap, they dominate.

“If and when that gap widens and tracker or discounted variable rates get near to one percentage point less than fixed deals, we’d expect the mix to shift and more borrowers willing to give up that security. But for now, with the rate outlook clouded by sticky inflation and global uncertainty, peace of mind is winning out.”

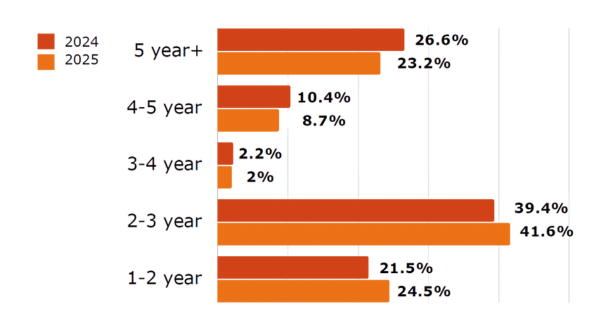

Product Length Preference

“Even though fixed rates dominate, borrowers are hedging their bets on how long to lock in for. Two-thirds of those who fixed in July chose deals lasting three years or less – up from just under 61% a year ago.

“That shows people still want the certainty of a fixed rate, but they increasingly want the flexibility to move if the cost of borrowing keeps edging down. For many households, a two- or three-year deal feels like the best of both worlds: protection from short-term volatility without being tied in if rates fall further over the next couple of years.

“It’s a trend that underlines how cautious borrowers remain about committing for the long haul. Confidence is returning, but the experience of the past few years has left many wary of getting stuck paying over the odds for their mortgage.”

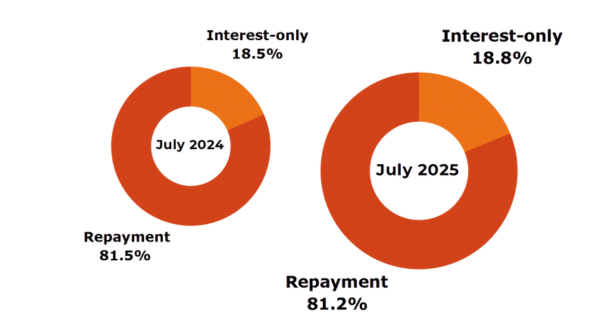

Repayment vs Interest-only

“Despite the affordability pressures of the past two years, there’s been no meaningful shift towards interest-only borrowing. In July, 81.2% of new loans were on a repayment basis – virtually identical to a year ago – showing that interest-only remains a niche part of the market.

“This stability shows new borrowers are committed to paying down capital from the start, not using interest-only as a workaround. It remains largely the preserve of wealthier borrowers with a clear exit plan, rather than a mainstream option. Most people prefer to tackle their debt head-on rather than defer it, even with mortgage rates much higher than in recent years.

“That said, all eyes will be on the FCA’s ongoing review of mortgage rules, specifically whether it decides to allow borrowers to use the sale of their property as an acceptable repayment vehicle. If that happens, it could open the door to more people exploring interest-only as an option.”

Purchase-Remortgage Split

“July’s lending mix, with purchase loans making up just 40.6% of activity – down sharply from 50% a year ago – points to a market still finding its feet after a period of heightened borrowing costs. While mortgage rates have fallen since last year, they remain significantly higher than a few years ago, keeping some would‑be purchasers on the sidelines.

“At the same time, 1.8 million fixed‑rate deals are set to mature this year. That’s driving a surge in remortgage activity as borrowers look to secure competitive deals or adjust their borrowing to fit changing circumstances.

“But with further rate cuts widely expected, the conditions are aligning for purchase lending to regain momentum in the months ahead. The summer and autumn could well see a renewed wave of buyers returning with fresh confidence, especially if borrowing costs fall further.”

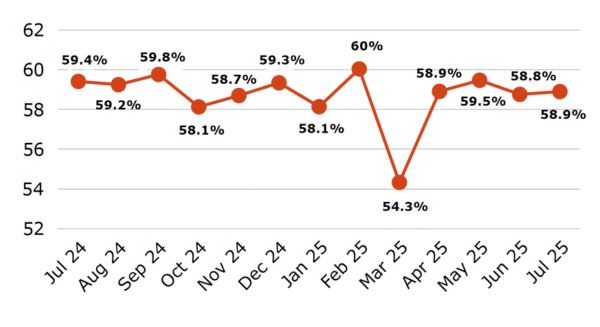

Average loan-to-value

“With the mortgage guarantee scheme now permanent, the Bank of England allowing lenders to provide more loans with higher loan-to-income ratios, and more flexible stress testing from some high street lenders – alongside lower rates and a drive to increase housebuilding, conditions are gradually improving for first-time buyers.

“If that leads to a greater number of first-time buyers getting their foot on the ladder – which it should – then we’re likely to see average LTVs, currently at 58%, edging up.

“That, in turn, could spark greater competition among lenders at the higher-LTV end, creating a virtuous circle for those wanting to get a foot on the property ladder.”

As market momentum builds and affordability begins to improve, the second half of 2025 promises opportunity—for movers, remortgagers, and advisers alike.

If you’re a mortgage and protection adviser looking to support your customers through these shifting conditions with a market-leading level of support and technology, contact us to discuss how our proposition can help.